Español

Español Download

Download Contact

Contact

MORE THANDISTRIBUTION2013 ANNUAL REPORT

C.E.O. Report on the 2013 RESULTS

GRUPO POCHTECA, S.A.B. DE C.V.

HIGHLIGHTS FOR THE YEAR 2013 INCLUDED:

- Increase in sales and EBITDA. Despite the overall fall of raw material prices and the contraction of the construction sector, sales and EBITDA grew 15% and 14%, respectively, mainly as a result of a 40% growth in sales volume and an increase in gross margins. This growth is significantly higher than the 1.06% growth in domestic GDP, than the 4.5% decrease observed in the manufacturing sector and the 0.6% contraction registered in the chemical industry.

- Acquisition of Productos Químicos Mardupol, a leading firm in the inorganic chemical products.The company was acquired on February 1, 2013. By February 5, 2013, redundant operations were closed or merged and the product portfolio, jointly with inventories and suppliers base, were integrated into Pochteca’s SAP system, in order for both Companies operations to operate seamlessly as a single entity.

- Brazil. The acquisition of Coremalwas completed on December 31, 2013. The Brazilian company is a chemical distributor with extensive coverage in the country. Impact in the profit and loss statement will only be felt in 2014, although, from a balance sheet standpoint, the full impact is reflected on Pochteca’s 2013 closing balance sheet.

- Solid financial position. Despite the acquisitions made in 2013, our balance sheet remains solid. We respected the financial guidelines ordered by the Company’s Board of Directors. Under that assumption, we recorded a Net Debt-to-EBITDA ratio of 2.2 times (considerning pro-forma 2013 EBITDA for Coremal).

- Risk Diversification. Our strategy to diversify customers, geographic markets, industries and products has been consolidated. The top five clients represented 9% of total sales. Similarly, our top five products represented 8% of total revenue and no customer or product represents more than 3% of sales while geographic and industry dispersion provides protection to the Company from industry or region specific problems.

2014 OUTLOOK

Mexico's energy reform will benefit our business.

- We expect the oil and gas exploration and drilling sectors to grow importantly in the following 18 to 24 months, as a result of energy reform. These niches represent more than 7% of our total sales, so we expect a rising demand for our products in these sectors.

- We expect that the reduction in the uncertainty of the supply of basic chemicals, gas and electricity and the gradual drop in the price of energy that will derive from energy reform will result in a sustained growth in investments in the chemical industry in particular and in general, in the manufacturing sector. This will generate growing demand for Pochteca’s products.

- Double-digit growth. The Coremal acquisition along with our organic growth, will enable the Company to grow in excess of 25% during 2013, not considering potential acquisitions that could be completed before the end of 2014.

- Other potential catalysts.The environment in 2013 for Pochteca was adverse in all major external variables: commodity prices going down, paralyzed public works, generalized contraction in construction and mining, among others. Any positive change in these variables will result in additional sales for the Company.

- We will continue evaluating potential mergers or acquisitions in the future. As we have been doing in the last two years, we will continually evaluate companies that could provide value to our shareholders our financial strength and a suitable risk profile.

CONSOLIDATED RESULTS

|

Consolidated |

January - December |

||

|---|---|---|---|

|

Millions of Pesos |

2013 |

2012 |

Var % |

|

Net sales |

4,473 |

3,896 |

15% |

|

Net income |

40 |

51 |

-22% |

|

EBITDA |

216 |

190 |

14% |

|

Net Debt-to-LTM |

220 |

0.29 |

|

Sales in the year grew 15% to Ps. 4,473 million. Gross income reached Ps. 749 million, a 20% increase against the Ps. 627 million figure recorded in the past year. Gross margin was 16.8% as percentage of sales against the 16.1% margin reached in 2012.

Income before taxes was Ps. 66 million, a 23% decrease against the figure recorded in 2012. This was the result of a foreign exchange loss of Ps. 30 million registered in the year in comparison with the Ps. 3 million foreign exchange gain recorded in 2012, thus leading to a Ps. 33 million adverse impact if compared with the previous year. Net income for the year was Ps. 40 million, which decreased 22% in comparison with the Ps. 51 million figure recorded in 2012. The adjustment in net income for the year was mainly due to the foreign exchange effect and higher taxes produced by having consumed accumulated tax losses in Dermet de Mexico during the year. However, EBITDA, which is not affected by conjunctural factors such as currency exchange fluctuations, increased 14% to Ps. 216 million, in comparison with Ps. 190 million in the previous year.

This growth was achieved despite several adverse factors that occurred during 2013. The most important were:

- The general fall in prices of raw materials sold by the Company. The slowdown in the world economy had a depressing effect on a number of raw materials internationally. High-volume products of Pochteca as sodium cyanide or titanium dioxide suffered double-digit price declines during the year. These decreases generated significant losses from holding inventories, in addition to generating lower sales per ton sold. Fortunately, we were able to increase the volume of tons sold in 42%, thus offsetting the fall in prices, achieving a 15% growth in total sales. Similarly, despite the considerable losses from inventories affected by downwardly adjusted prices, gross margin as percentage of sales grew from 16.1% to 16.8%.

- Oil exploration and drilling customers had a very difficult time collecting from their customers. This created constant delays in payments to Pochteca from these customers. Having these customers constantly in arrears dampened sales volume to them as well as putting pressure on the Company’s receivables. This situation inevitably affected Pochteca negatively, given that over 7% of the Company’s sales go to oil and gas.

- The decline in the construction activity heavily affected an important sector of Pochteca’s clients such as paint, lacquer coatings and construction materials manufacturers. These customers make an important part of the revenue of the Company’s Solvents, Blends and Coatings segment. This segment epresents 29% of Pochteca’s sales. Similarly, the weakness in construction and infrastructure projects impacted negatively on the sale of lubricants and greases. The underspending of the Government budget affected these sectors in particular and the industry in general, thus affecting demand. The fall in prices for minerals, which affected both the prices of raw materials used in mining (i.e. cyanide and gold) the volumes required by the mines of these raw materials, as well as the production levels of the mines.

- Our Company continued to consolidate its risk diversification model. The five major customers went from 11.6% of sales in 2012 to a 9.4% contribution in 2013, with none reaching 3% of total sales. Similarly, the top five products accounted for 8.3%, none reaching 3% of sales. Diversification of geographical markets and industries reinforced this risk dispersion and allowed the Company to move from shrinking to stable, growing industries, as well as moving from declining demand of products to a more dynamic portfolio. These strategic movements allowed us to increase sales and maintain margins, in spite of a contractionary economic environment and deflation in most of our product lines.

The fact that the Company was able to grow at double digit rates, increase its gross margins and maintain a healthy and stable balance of receivables during 2013 leads us to believe that the diversification of products, customers, industries and regions implemented in recent enhanced the Company’s resilience and capacity for adaptation. This model minimizes the impact of adverse market conditions.

Under a less diversified risk model, a significant difficulty in one or two major markets or customers could result in severe sales and margin contractions that could potentially affect the profitability and solvency of the Company in a permanent way.

This diversified model will allow the Company to capture significant benefits once the energy reform will be consolidated. The positive impact will be seen not only in the industrial sectors of oil exploration and drilling, which represent a significant portion of the Grupo Pochteca’s sales, but also in investments to be made in more than 30 industries connected with the use of products derived from oil, gas and/ or electricity as energy inputs. All these industrial branches are served by Grupo Pochteca. The growth experienced by these markets will result in an increase in the demand of the Company’s product portfolio.

Accumulated sales grew 15%against the previous year, despite the fact that the weighted average price of our portfolio of products contracted more than 16% in the year in comparison with 2012.

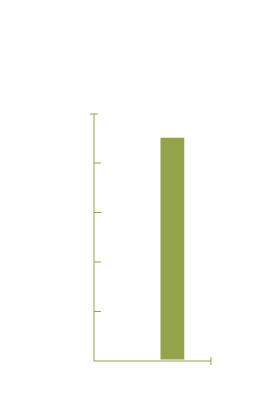

GROSS MARGIN AS PERCENTAGE OF SALES

|

ACCUM. 12 |

|

ACCUM. 13 |

|---|---|---|

|

16.1% |

Gross margin |

16.8% |

EFFICIENCY AND PRODUCTIVITY

Accumulated EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) was Ps. 216 million in 2013, representing a 14% increase against the previous year.

Operating expenses as percentage of sales were 11.9% in comparison with the 11.2% margin observed in the previous year. This deterioration was mainly the result of the decline in the price of products. In order to be able to grow 15% in our sales, we had to sell 42% more tons than the previous year. Distribution this additional volume requires more resources in most important areas of the company.

We are confident that we can reduce operating expenses as a percent of sales, as sales continue to grow and the rate of decline in prices of raw materials is reduced.

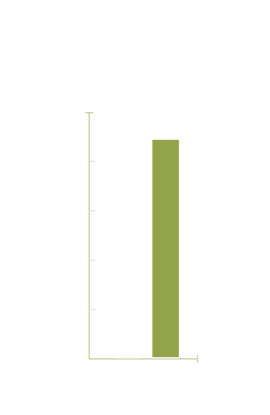

OPERATING EXPENSES (EXCLUDING DEPRECIATION)

|

ACCUM. 12 |

|

ACCUM. 12 |

|---|---|---|

|

11.2% |

Expenses / sales |

11.9% |

FINANCIAL EXPENSES AND FOREIGN EXCHANGE GAIN

Financial expenses for the year were Ps. 59.8 million, which favorably compares with the Ps. 71.7 million recorded in 2012, representing a 17% decrease in the year.

As per the foreign exchange position in the year, the Company registered a loss of Ps. 29.6 million, which if compared with the gain of Ps. 3.5 million observed in the previous year, results in a Ps. 331.1 million adverse effect in comparison with 2012.

CASH GENERATION

On a pro-forma basis, considering the Mardupol results as if these were consolidated beginning December, 2012, the Company’s cash generation for the year was (Ps. 213 million). This was mainly affected by capital expenditures of Ps. 208 million. Investments included a new site in Queretaro for our technology information systems and a backup site in Mexico City, in addition to improvements made on Mardupol’s tanks and warehouses. Through these actions the Company is well positioned in terms of infrastructure for the years to come. Capital expenditures of Ps. 80 million are projected to occur in 2014, as most of resources have been already invested during 2013.

BALANCE SHEET

WORKING CAPITAL

In spite of the generalized arrears in the oil and gas sector and in spite of the severe contraction in the construction industry the Company reduced the collection period of its receivables from 54 days at the end of 2012 to 53 in the same period of 2013. In addition, inventory ratio changed from 70 to 71 days, and supplier’s payment term remained steady at 92 days. The previously mentioned ratios include exclusively figures for Pochteca without Coremal. The latter was incorporated into the Company’s balance sheet on December 31, 2013, so its sales, expenses and profits did not impact Pochteca during 2013, and thus, are not considered for this calculation.

NET DEBT

Net debt was Ps. 623 million at the end of 2013. The figure includes Coremal'sank debt as well as the debt contracted by Grupo Pochteca for the acquisition of Coremal. The Net Debt-to-EBITDA ratio includes Grupo Pochteca’s EBITDA plus EBITDA from Coremal on a pro-forma basis, given that Coremal'sP&L is not consolidated for 2013. .

Net Debt-to-EBITDA was 2.2 times at the end of the quarter, which is marginally higher than the 2.0 times established as an internal goal. After the implementation of commercial strategies to increase sales throughCoremal's operation, and the optimization of working capital financing in Grupo Pochteca and Coremal, the ratio is expected to return to around 2.0 times.

Interest coverage ratio remained at 2.61 times at the end of the year, practically the same ratio observed in 2012 after taking into account the effect of the Mardupol and Coremal acquisitions in 2013.

|

Consolidated |

January - December |

|

|---|---|---|

|

Millions of Pesos |

2013 |

2012 |

|

Net Debt |

623 |

55 |

|

Net Debt-to-LTM EBITDA |

2.20 |

0.29 |

|

Interest Coverage |

2.61 |

2.61 |

|

Outstanding Shares |

130,522,049* |

621,891,141 |

*After reverse stock split (5-to-1)

DISCONTINUED OPERATIONS

In 2012, the Company recorded the Central American and Brazilian subsidiaries as discontinued operations, after the Board decided to sell them off, in light of the fact that their contribution to EBITDA was less than 10% of total EBITDA. This would allow the Company’s management to focus on the main EBITDA generating businesses. During the summer of 2013, largest subsidiary, Pochteca Brazil, was sold. Conversely, we were unable to sell Guatemala, Salvador and Costa Rica mainly due to the reduced scale of their operations (combined sales of Ps. 167 million). Following our external auditor advice and given the unlikelihood of selling them, the Company reincorporated these three operations into the business. In order for the 2012 and 2013 numbers to be comparable, the financial information for 2012 has been modified so as to include the unsold operations for the years 2012 and 2013, on the ordinary course of the business, including the financial statements of the Company. Total revenue generated by these three operations was Ps. 198 million in 2013, a 19% increase in comparison with the previous year.

COREMAL

On December 31, 2013 the purchase of 100% of the shares of COREMAL was completed. It included COREMAL was completed. It included Coremal – Comercio e Representações Maia Ltda., Mercotrans Tansportes e Logistica Ltda. and Coremal Química Ltda. On a first stage, 51% of the business is paid for while the remaining 49% is paid in five annual installments of 9.8% of the value of the company, utilizing the same valuation methodology as in the first stage, but based on the results achieved in each subsequent year. This scheme secures an alignment of interests between Coremal's shareholders and Grupo Pochteca for the next five years.

Coremal was founded in 1952. Currently, it is one of the largest chemical products distributors in Brazil. It has six distribution centers along the country. The company’s infrastructure supplies packaged and bulk products to over 8,600 customer in the 27 states of the country, through the support of its subsidiary Mercotrans Transport and Logistics, Ltd.

The market for chemicals and lubricants in Brazil is significantly larger than the Mexican market. Its complexity and local characteristics, however, lead us to operate through an experienced Brazilian partner with proven track record in the sector. Grupo Pochteca believes that Coremal represents a very positive acquisition. Purchasing a well-known group with proven managerial abilities and that has a nationwide distribution network and long term relationships with world class suppliers and that operates under the most stringent HSSE standards with a client, market, product and regional diversification that is consistent with Pochteca’s strategy, is the best way to enter the Brazilian market. Coremal operates following the best HSSE industry practices and has been certified by the Associquim (Association of Chemical Industry of Brazil).

Among other things, the transaction allows Pochteca to:

- Consolidate its presence in Latin America, through which it adds value to major manufacturers and multinational customers in search of regional distributors.

- Enter into the chemical and lubricants distrbution segment in Brazil. The market is much larger than Mexico’s (chemical products consumption in excess of US$ 70 billion per year). In addition, the market is more fragmented than the Mexican market.

- Export know-how and complementary products to Coremal’s portfolio and vice versa.

As in other transactions, the Company kept conservative Net Debt-to-EBITDA and interest coverage ratios to limit the risk profile of the business.

INDEPENDENT ANALYST AND FINANCIAL COVERAGE ON GRUPO POCHTECA

Grupo Pochteca signed in to the Independent Analyst Program. The Selection Subcommittee agreed to assign CConsultora 414, S.A. de C.V. ("CONSULTORA 414") as the analysis firm responsible for covering the securities of POCHTECA.

Other analysts that follow the Company’s stock are Actinver Casa de Bolsa, Vector Casa de Bolsa and BBVA Bancomer..